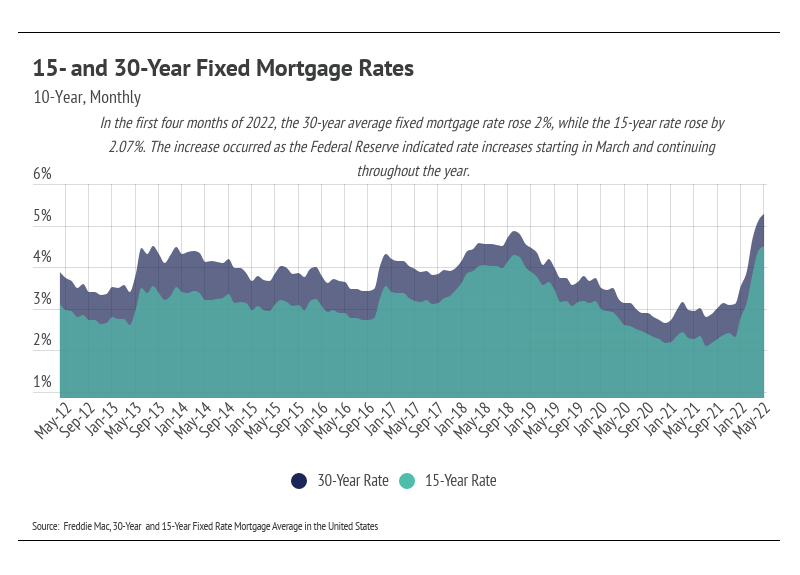

After the Fed’s May meeting, Fed Chair Jerome Powell announced that they are raising their benchmark rate by 0.50%, the largest hike since 2000. Earlier this year, the Fed was expected to raise interest rates by 0.25% at least six times this year, going from 0% to 1.90%. Now that each increase will most likely be 0.50%, the market expects the federal funds rate to reach 2.75% to 3.00% by the end of the year, which would be the highest in 15 years. Although the fed funds rate doesn’t directly affect mortgage rates, the rate hike moves into the broader economy quickly. Over the past four months, mortgage rates have moved about 2% higher for both 30- and 15-year fixed mortgages. Economists now estimate that 30-year mortgage rates could climb above 6% by mid-2022, which is fast approaching. Because the Fed indicated the path of rate hikes for the rest of the year, we expect mortgage rates to top out at around 7% this year for prime borrowers.

A rising rate environment increases short-term demand as buyers try to lock in lower mortgage rates, which is what we are seeing now. The increased short-term demand is driving prices right now outside of supply, which begs the question: Will higher mortgage rates actually drive down prices? No, they sure won’t.

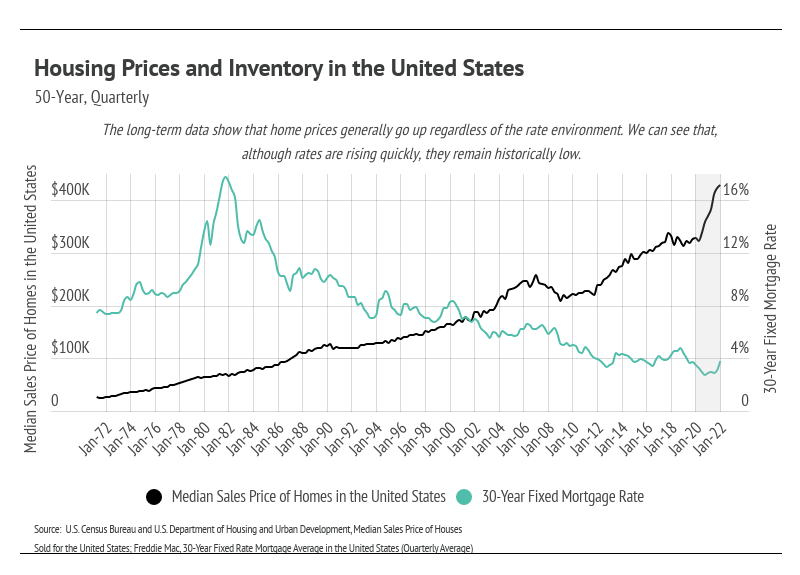

Using history as our guide, we can see that home prices continued to rise even as mortgage rates peaked at over 18% in the 1970s, which would translate to about $7,500 per month on a $500,000 loan. Luckily, we aren’t going back to those rates. Higher rates, however, will do exactly what the Fed intends, which is to take money out of the economy and decrease overall demand. The average 30-year mortgage rate was 3.11% in December 2021, rising to 5.10% by the end of April 2022. If you bought a home in December and financed it with a $500,000 mortgage loan at 3.11%, your monthly spend on principal and interest would be $2,138 — versus $2,715 if you got the same loan in April 2022 at 5.10%. Over the life of the loan, you’ll spend $207,720 more at 5.10%. From the Fed’s perspective, that equates to roughly $500 less per month to spend on goods and services, bringing down aggregate demand when we multiply that reduction of disposable income across households. The gradual rate increases are meant to avoid sending the economy into a recession.

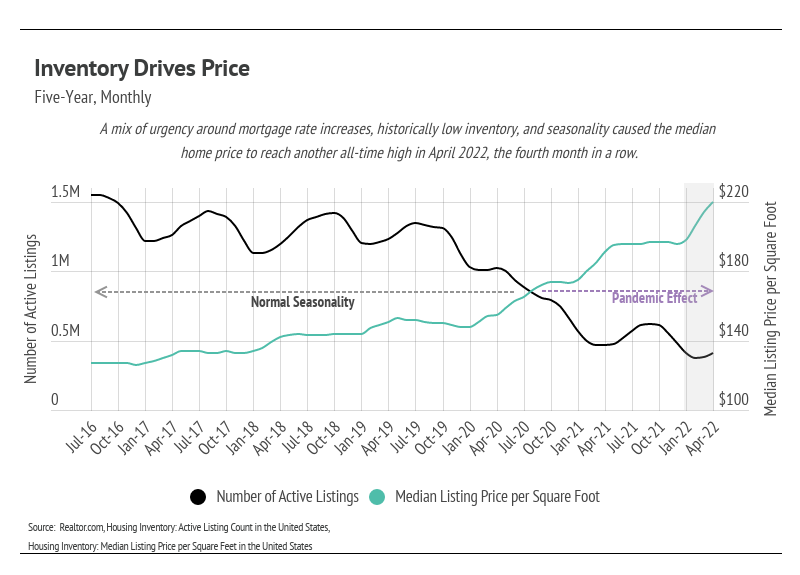

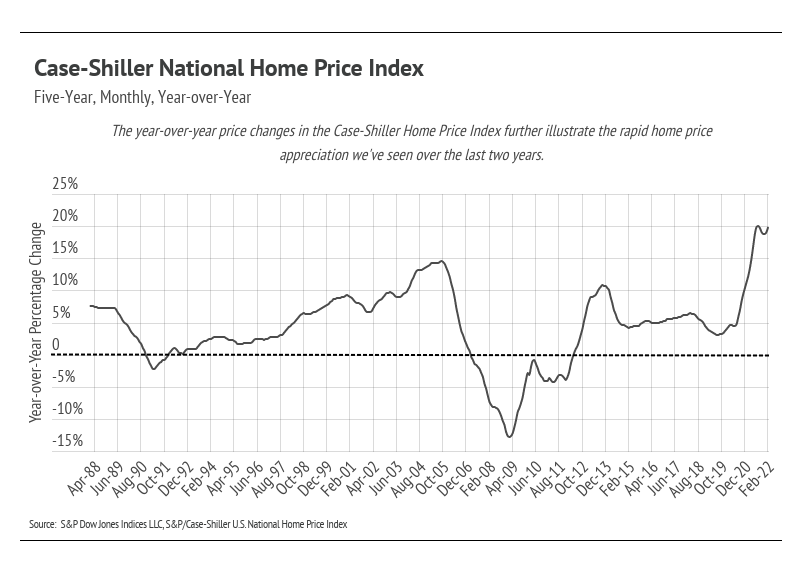

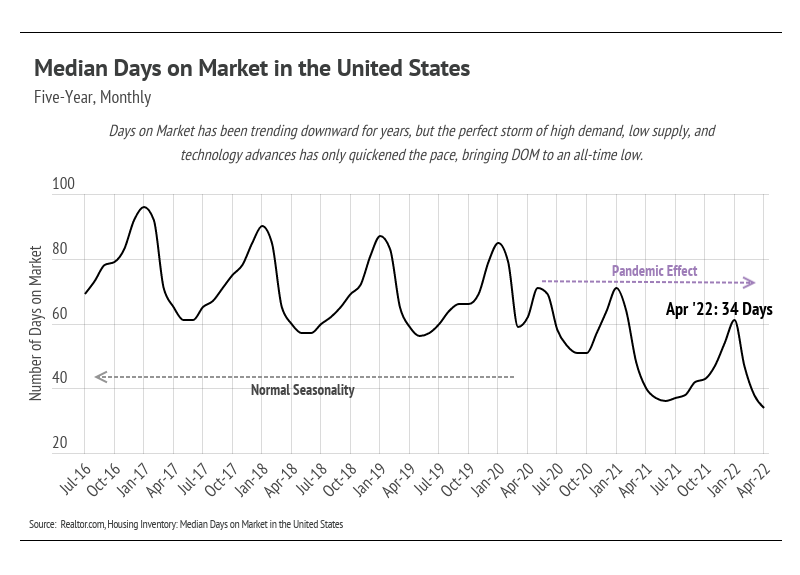

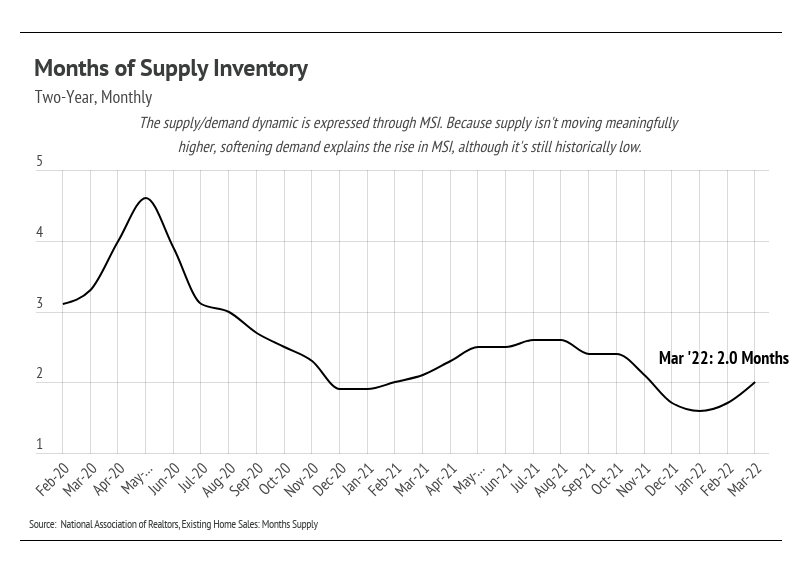

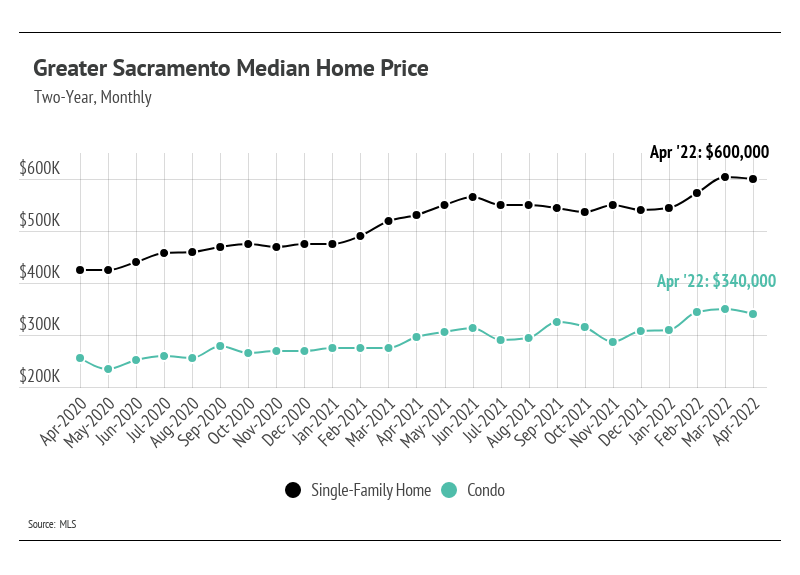

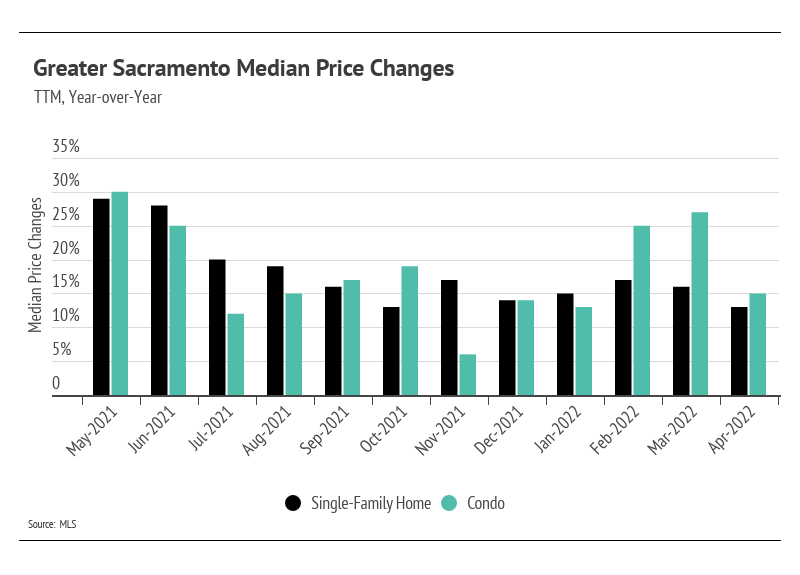

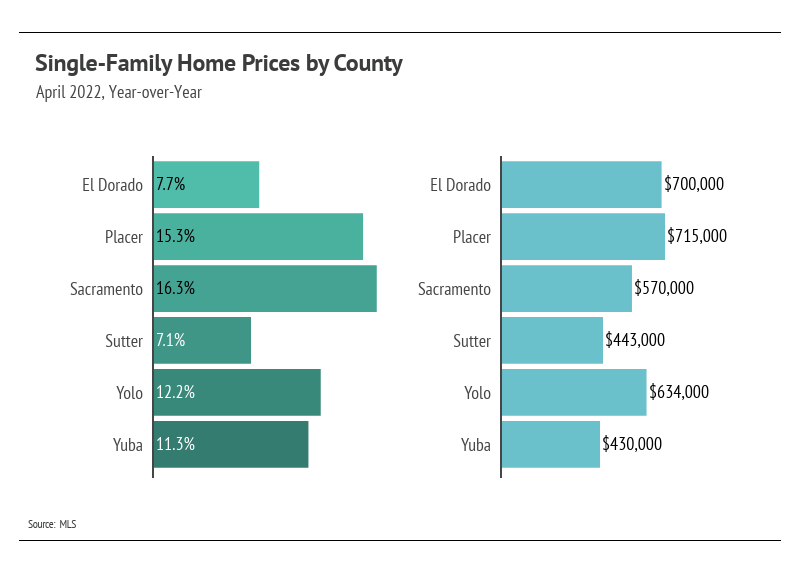

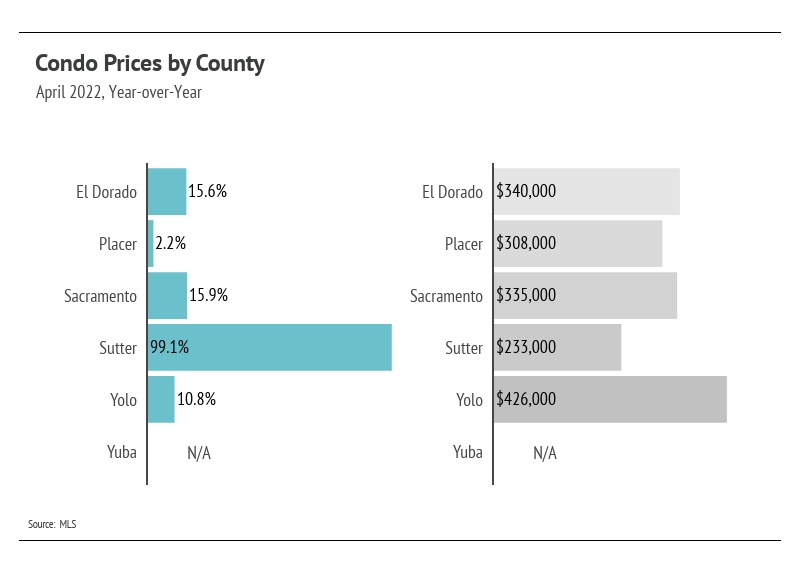

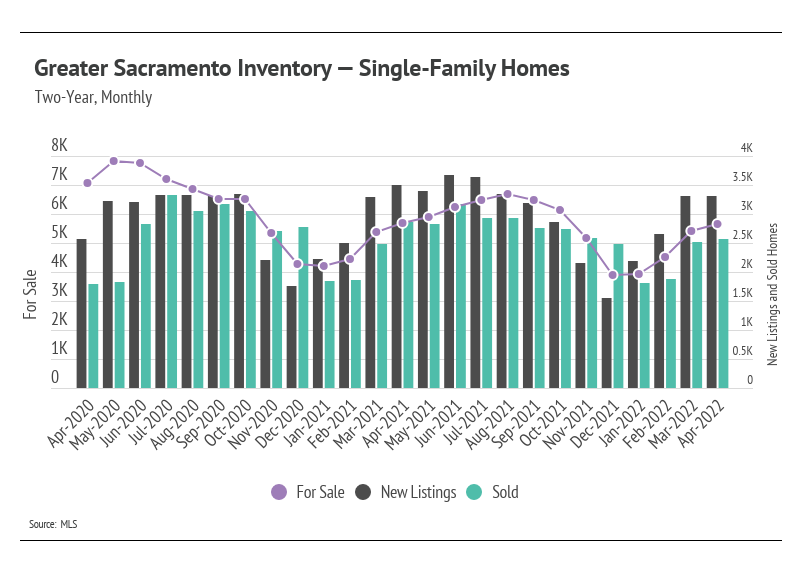

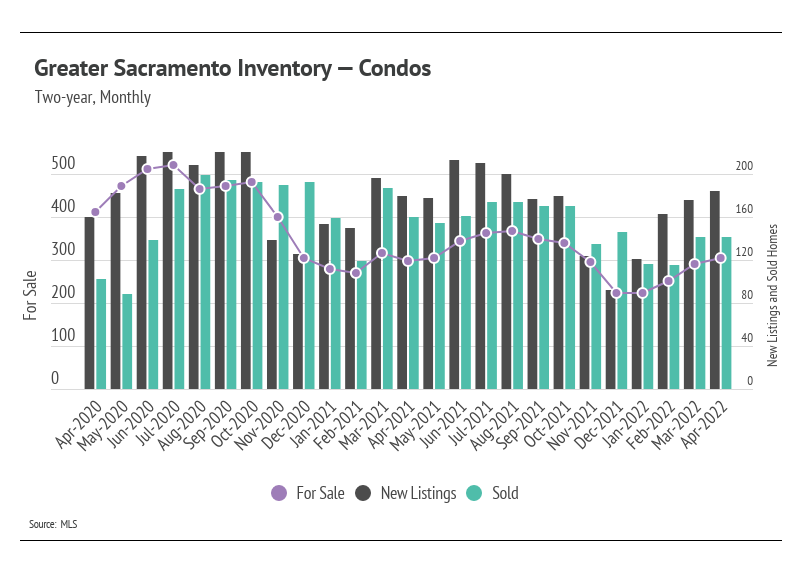

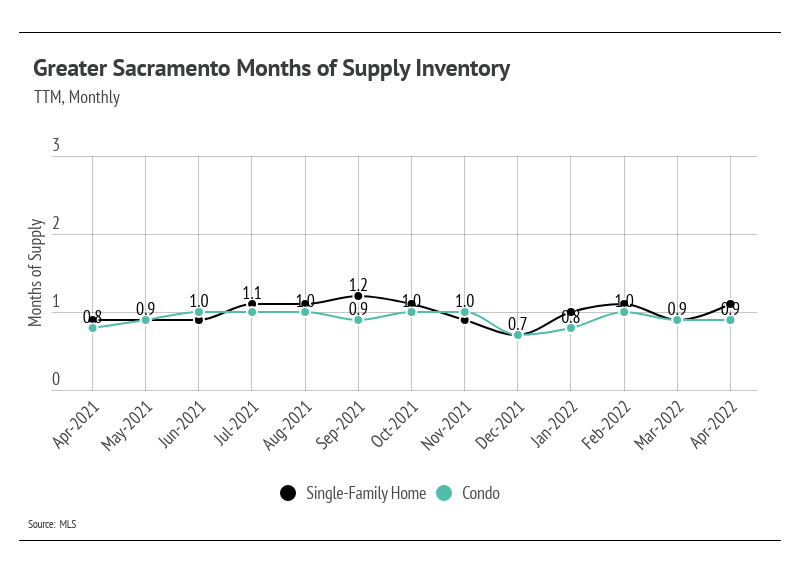

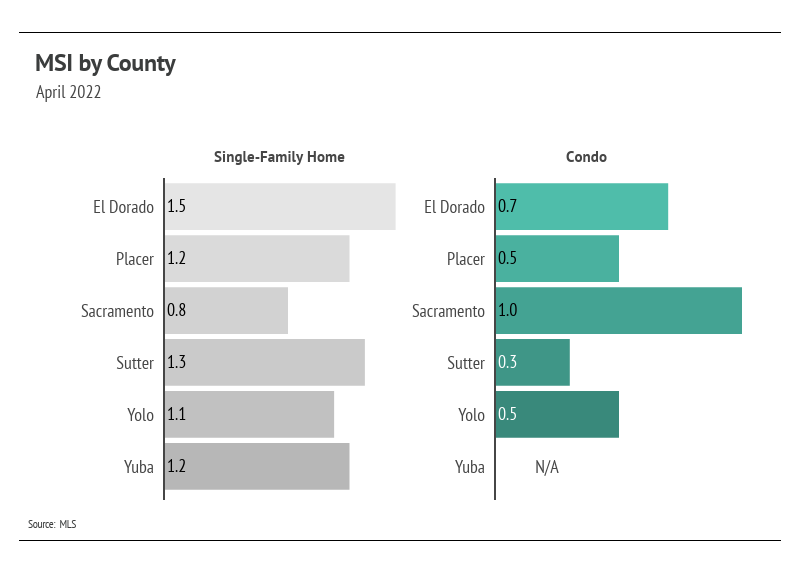

In addition to rising rates, supply still drives home prices. In April, the housing supply ticked up ever so slightly, but it’s still 60% lower than the number of homes on the market in April 2020. We are entering what is traditionally the hottest time of year for the housing market with a record low supply of homes. Over the past four months, which had the lowest inventory on record, home prices increased 12%.

If you are considering buying a home, there aren’t many reasons to wait. Home prices and rates are still rising. The low supply continues to make the market extremely competitive. We are starting to see some softening in demand, but not nearly enough to balance the supply side of the market. |

|